If you lease or store goods, understanding what is a bailment under the Personal Property Securities Act 2009 (PPSA) is crucial to protecting your assets in legal disputes. Regarding the matter of legal bailments, in this blog we take a close look at the case Bredenkamp v Gas Sensing Technology Corporation (GSTC), in the matter of Welldog Pty Ltd (In Liq) (Receivers and Managers Appointed) [2017] FCA 1065, to help businesses navigate PPSA complexities.

While the outcome of this case is interesting, all bailment circumstances are different. So please don’t hesitate to seek advice from our Sydney business lawyers on 1800 770 780.

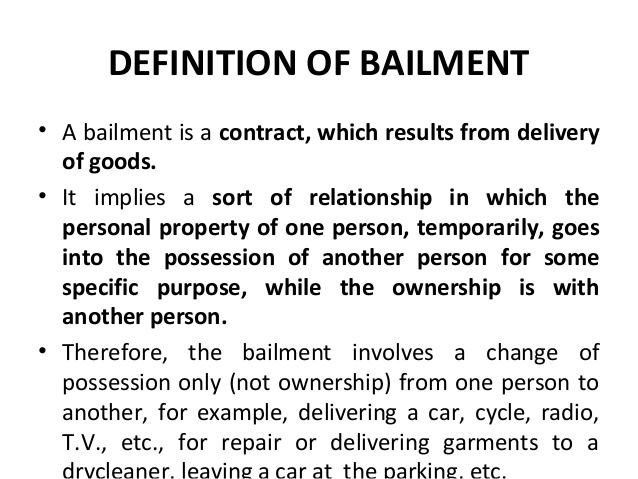

What is a bailment?

Bailment definition: Bailment is a legal relationship in common law where physical possession – but not ownership – of personal property is transferred from one person to another. In Australia, bailments can be classified into several categories based on their nature, legal obligations, and purpose.

Types of bailments

Gratuitous Bailment (Without Payment)

Gratuitous Bailment definition: Occurs when the bailee receives possession of goods without providing any consideration (payment or service). The arrangement is based on goodwill rather than a contractual obligation.

Legal implication: The bailee has a duty of care but may have limited liability if the goods are damaged.

Bailment for Reward (Commercial Bailment)

Bailment for Reward definition: In this type, the bailee pays the bailor or provides a service in exchange for possession of the goods. This is common in commercial agreements.

Legal implication: The bailee has a higher duty of care since they are receiving compensation. If they fail to return the goods or damage them, they may be liable.

Pledged Bailment (Security Bailment)

Pledged Bailment definition: Occurs when goods are given as collateral for a loan or debt, meaning they can be sold if the debtor fails to repay.

Legal implication: If the debtor defaults, the bailee (lender) has the right to sell the goods to recover the debt.

Bailment for Storage or Safe Custody

Bailment for Storage definition: In this case, the bailee is responsible for keeping the goods safe, usually for a fee. The bailee does not use the goods but ensures their security.

Legal implication: The bailee must prevent loss or damage, or they may be held liable.

Constructive Bailment (Implied Bailment)

Constructive Bailment definition: Can arise without a formal agreement, based on circumstances. If someone takes possession of goods and assumes responsibility, an implied bailment exists.

Legal implication: The bailee must take reasonable care of the goods but may not have the same legal obligations as in a contractual bailment.

Involuntary Bailment

Involuntary Bailment definition: Can happen when someone unintentionally comes into possession of another person’s goods but still has a duty of care.

Legal implication: The bailee should attempt to return the goods or contact the rightful owner.

Bailment for Hire (PPS Lease Bailment Under the PPSA)

Bailment for Hire definition: If goods are leased for more than two years, the arrangement may fall under the PPSA as a Personal Property Securities (PPS). The bailor must register their interest in the Personal Property Securities Register (PPSR) to protect ownership rights.

Legal implication: If the bailor fails to register the lease on the PPSR, they risk losing ownership if the bailee becomes insolvent.

What is a PPS lease?

PPS lease definition: PPS lease refers to a Personal Property Securities (PPS) lease, which is a type of lease covered under the PPSA. This law governs security interests in personal property, including leased or hired goods. A PPS lease applies to certain leases or bailments of personal property (not land, buildings, or fixtures) where the lease period:

- Is for more than two years; or

- Has a term of up to two years but automatically extends beyond two years.

The owner (lessor) should register the security interest on the PPSR to protect their rights. If the interest is not registered, the lessee may claim ownership if they default or become insolvent.

Bailment Under the PPSA

Bailment under the PPSA, refers to an arrangement where one party (the bailor) delivers goods to another party (the bailee) for a specific purpose, while ownership remains with the bailor.

When is Bailment Under the PPSA?

For a bailment to be subject to the PPSA, it must meet the following conditions:

- The bailor retains ownership: the person providing the goods (bailor) still owns them, even though another party (bailee) has possession.

- The bailment is for value: the bailee must provide some form of consideration (e.g., payment or a commercial benefit), although certain arrangements can still be covered even without direct payment.

- The bailment meets the definition of a PPS lease.

If these conditions apply, the bailor must register their interest on the PPSR to protect their ownership rights.

Why Does Resgistration Matter?

If a bailor fails to register their interest on the PPSR, they risk losing ownership if the bailee becomes insolvent or bankrupt. In such cases, creditors may claim the goods, leaving the original owner with no legal claim.

Case Summary: GSTC & Welldog – PPS Lease Dispute

Parties Involved:

- GSTC (US company) – Provided product line management and R&D services.

- Welldog (Australian subsidiary) – Stored GSTC’s equipment at its Toowoomba base.

- Liquidators & Receivers – Disputed ownership and security interest in the stored equipment.

Nature of the Arrangement:

- GSTC shipped equipment from the US to Australia.

- Welldog stored the equipment for GSTC until it was required for GSTC’s work in Australia.

- This occurred at least four times, and Welldog had possession of the equipment.

Key Legal Issue:

- After Welldog went into administration and liquidation, the liquidator sought to retain the equipment for the benefit of unsecured creditors, arguing it was subject to a PPS lease under s 13 of the PPSA.

- If it was a PPS lease, GSTC needed to have registered its security interest; otherwise, under s 267 of the PPSA, the equipment would vest in Welldog’s liquidators.

Arguments:

Liquidator’s Position:

- The arrangement was a PPS lease requiring registration.

- GSTC failed to register, meaning the equipment should be available to unsecured creditors.

Receivers’ Position:

- A PPS lease requires a bailment for value, and GSTC was not regularly engaged in bailing goods (s 13(2)(b) PPSA).

- The case predated the May 2017 PPSA amendments, which abolished the rule that a bailment for an indefinite term is automatically a PPS lease.

Key Takeaways:

- The case revolved around whether the storage arrangement met the definition of a PPS lease.

- The critical issue was whether GSTC was in the business of bailing goods, as required under s 13(2)(b) of the PPSA.

- The outcome would determine whether the equipment remained GSTC’s property or vested in Welldog’s liquidators for unsecured creditors.

What happened in this case?

GSTC, a US company, provided product line management and research and development services.

It was common for its Australian subsidiary, Welldog, to store equipment shipped from GSTC in the US, to be used by GSTC subsequently when work was to be done by GSTC in Australia. This happened on at least four occasions. The equipment was stored at the Toowoomba base of Welldog Australia. It was not in dispute that Welldog had possession of the equipment.

GSTC conducted its own operations in Australia, often alongside Welldog. Receivers were appointed to Welldog which subsequently passed into administration and liquidation. The liquidator sought to retain possession of the goods (equipment) for the benefit of unsecured creditors, arguing that it was the subject of a PPSA lease under s 13 of the Personal Property Securities Act 2009 (PPSA) requiring registration to avoid the application of s 267 of the PPSA.

The Receivers, on the other hand, argued that the arrangement could only be a PPS lease if it was a bailment for value and the bailor (GSTC) was regularly engaged in the business of bailing goods – s 13 (2) (b) PPSA. The facts of the case pre-date the May 2017 amendments abolishing the stipulation in section 13(1)(b) that a bailment for an indefinite term is a PPS lease.

Was there a bailment?

GSTC could demand return of the equipment to it or to its employees or agents, at any time. There was no contractual arrangement for example, by which Welldog could insist on retaining possession of the property.

Such arrangements where the bailor can at any moment demand return of the object ‘bailed’ are called gratuitous bailments.

But Welldog did not hold the equipment exclusively for GSTC. Some of the equipment which was stored was used by Welldog, even though other parts, or sometimes even the same parts, were used by GSTC. Nevertheless, the court concluded that the facts still qualified the arrangement as a common law gratuitous bailment despite the fact that Welldog did not hold the equipment exclusively for GSTC.

Was GSTC regularly engaged in the business of bailing “personal property”? Courts Reasoning – Step-by-Step Analysis

- Nature of Equipment Storage

- The court observed that Welldog stored the equipment while GSTC was in transit between projects.

- When GSTC required the equipment for a new job or task, it would retrieve and use it accordingly.

- Frequency and Pattern of Storage

- While GSTC had conducted hundreds of geochemical analyses worldwide, the storage arrangement with Welldog only occurred four times.

- The ad hoc nature of these instances suggested that storing equipment was not a normal or structured part of GSTC’s business operations.

- GSTC’s Business Model

- GSTC’s primary business was providing services using skilled personnel and specialised equipment.

- The company did not make a profit from bailing its equipment to Welldog or to Welldog’s clients.

- No Consideration for Bailment

- GSTC did not receive a fee from Welldog for the storage or use of the equipment.

- Even if GSTC had received payment, it would have been an incidental expense, not a core revenue-generating activity.

- Welldog’s Use of the Equipment

- While Welldog occasionally used the equipment, and this may have generated some income for GSTC (as Welldog was its subsidiary), there was no structured business model in which GSTC regularly bailed goods for profit.

- Distinguishing Business Arrangements from Bailment

- The court noted that any financial benefit arising from Welldog’s use of GSTC’s equipment resulted from a service provision arrangement rather than an indication that GSTC was in the business of bailing goods.

- Final Conclusion

- Based on these findings, the court determined that GSTC was not regularly engaged in the business of bailing goods, as required under s 13(2)(b) of the PPSA.

- Consequently, the storage of equipment did not constitute a PPS lease, meaning GSTC was not required to register a security interest under the PPSA.

Understanding “value” under the PPSA

Under the PPSA, the concept of “value” is crucial in determining whether an interest in goods qualifies as a PPS lease or security interest. Below are key insights into what qualifies as “value” and what does not, referencing specific sections of the PPSA.

What Qualifies as “Value” Under the PPSA

- Consideration Provided (s 10, PPSA)

- “Value” is broadly defined in s 10 as including the provision of consideration, which can be monetary or non-monetary.

- Consideration can include payment, contractual obligations, or other tangible benefits.

- Monetary Payment or Fees

- If the bailee pays a fee or provides financial compensation for the possession of goods, it constitutes value under the PPSA.

- Example: A company leasing equipment and paying a monthly rental fee to the owner.

- Obligations Under a Contract (s 12, PPSA)

- If the bailee enters into an agreement where they undertake obligations in exchange for possession of goods, this is recognised as value.

- Example: A contractor borrowing construction machinery under a contract requiring them to return it in specified condition.

- Indirect Economic Benefit

- Even if no direct payment is made, a commercial arrangement where the bailor receives a clear economic benefit (e.g., an increased share of revenue, reduced costs) may qualify as value.

- Example: A supplier providing machinery to a subcontractor in return for a share of profits from completed projects.

What Does NOT Qualify as “Value” Under the PPSA

- Mere Possession Without Obligation

- If a bailee has possession of goods without providing consideration, it is not a PPS lease under s 13(2)(b).

- Example: A parent company storing equipment at a subsidiary’s premises without any payment or contractual obligation.

- Incidental Arrangements

- If storage or use of goods arises informally and without a structured agreement, it does not constitute a bailment for value.

- Example: A business temporarily storing equipment at a third party’s premises without any formal leasing arrangement.

- Internal Transfers Within a Business Group

- When assets are transferred or shared between related entities without a formal leasing structure, it does not qualify as value.

- Example: A multinational corporation moving machinery between subsidiaries for operational efficiency.

- Free-of-Charge Lending or Storage

- If goods are provided gratuitously, such as a company lending equipment for free, no value is exchanged under the PPSA.

- Example: A supplier lending a display unit to a retailer for promotional purposes.

Did Welldog provide value for the bailments?

This element is required by s 13 (3) of the PPSA. The court considered it in the event that its conclusion as to the application of s 13 (2) (b) was wrong.

The word ‘value’ as used in s 13 (3), is defined in s 10 and

- a) means consideration sufficient to support a contract; and

- b) includes an antecedent debt or liability.

GSTC charged Welldog a management fee for the assistance it provided Welldog, and whilst Welldog issued invoices to GSTC for the completion of works using the equipment, no specific charge was invoiced to GSTC by Welldog for the bailments.

However, the receivers argued that this was not to the point. The issue, according to the receivers, was whether looking at the entire nature of the bailment relationship, value was given by Welldog as bailee, to GSTC as bailor. In other words, the receivers argued that “value” meant “value at large”.

It was clear that Welldog derived a benefit by reason of the equipment being at the Welldog premises. And it was Welldog’s obligation to ensure that the equipment was safely and securely stored in its secured premises. But it was not disputed that Welldog did not provide any specific value to GSTC for the bailment.

The court said that mere storage of the equipment safely and maintaining it in good working order was not evidence of value being provided by Welldog for the bailment. The court said it was to be expected of a subsidiary that it would keep the equipment of its parent safe even if it is not a bailee.

The court concluded that whilst the provision of relevant equipment by GSTC to Welldog was to enable Welldog to conduct its business with financial benefit potentially flowing to GSTC, value of such an indirect nature, including the management fee, does not satisfy the statutory concept of “value” as appears in s 10.

The court supported its conclusion by stating that the consideration was quite uncertain and it was too indirectly related to the provision of the equipment to support the ready conclusion that the equipment was bailed for such benefits.

His honour was guided by the New Zealand Rabobank and the Western Australian Re Arcabi decision in coming to this conclusion.

Protect your business with expert legal advice on bailments

If you are in the business of hiring or consigning your goods, or you otherwise part with possession of your inventory before payment, to safeguard your assets from unintended consequences under the PPSA, you must take proactive steps in managing bailments and security interests.

You can do so by ensuring that all long-term bailments or leases are properly documented, including clearly defining whether consideration (value) is provided can help mitigate risks.

Where a bailment may qualify as a PPS lease, you should register your security interest on the PPSR to protect ownership rights in the event of insolvency. Additionally, implementing clear contractual terms, including specifying storage conditions, return obligations, and financial arrangements, reduces ambiguity.

By adopting these measures, you can avoid unintended loss of assets, maintain legal control over your property, and ensure compliance with the PPSA.

If you would like more specific information, give Leigh Adams a call on 1800 770 780. He can review your arrangements to minimise the chances of losing it to your customer’s liquidator. As one of the most experienced commercial law firms Sydney has to offer, Owen Hodge Lawyers are well equipped to handle any and all of your civil litigation issues.